The tax system in Poland has already become a legend because of its casuistry and detachment from the realities of business. One example is the method of settling exchange rate differences required by the tax authorities, and specifically settling the value of foreign currencies held in the bank when withdrawing them paying contractors or other payments.

In general, legislators require this money to be stored in its historical value on the date of its receipt, and this historical rate and value should be confronted with the current bank exchange rate when withdrawing, to settle exchange differences between them. The regulations also stipulate that units of this currency must be settled in some order defined in the company's Accounting Policy, but for years it has been common practice that during tax inspections officials expect it to be according to FIFO - the oldest payments are settled the earliest.

Theoretically, companies that annually audit their books by a certified auditor can choose a generally worldwide accepted accounting method based on revaluation of monetary items, but among those using Odoo, few entrepreneurs are large enough to do so. In other countries, periodic revaluation of foreign currencies and the valuation of currency assets according to a simple weighted average value are normal practice, in Poland it is practically a privilege available only to a few. So imagine that you manage a warehouse with currencies, and you settle each "piece" of foreign currency with the price of its "purchase".

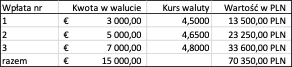

For example, a company received three payments from its recipients:

If the company then wants to pay the supplier EUR 10,000, it must successively settle exchange differences on each payment held, taking into account the bank payment rate and historical payment rates, i.e.:

Some accountants even enrich it by separately accounting partial profits for tax revenues and losses for costs. Whole this method generates a lot of unnecessary and valueless work, but dura lex, sed lex. Probably all accounting software packages developed in Poland have this functionality - their authors have long been skilled in overcoming legal reefs and shallows not encountered in any normal tax system. Some foreign software brands have also developed additional functionalities to help them work on the Polish market.

At Trilab, we are preparing to implement a module that will support this process, too.

Such adaptations to the completely unreasonable oddities served by national regulations absorb a lot of time that we could spend on solutions that improve our clients' business, but we do not want to leave our Clients with such a gap. And for now, we also suggest to look around in the Internet searching for interpretations published by experts and tax advisors. It may turn out, that the magical requirement of determining the "sequence" of withdrawing currency units may also be fulfilled by adopting AVCO method of valuation of these current assets to the company accounting policy.

Aktualizacja: za informacja w Rozliczanie Wartości Rozchodu Walut Obcych Według „FIFO” mechznaim automatycznego rozliczania rostał zbudowany.

Withdrawing currencies from bank accounts